Free early access

Keep rental income, expenses, receipts and EOFY records together

Landlord Wise is free during early access. Use it to organise rent income, expenses, receipts, documents and property records before tax time.

At a glance

- ATO definition: negative gearing occurs when rental income is less than deductible expenses, including interest on borrowings.

- Tax result: the ATO says a net rental loss may arise and may be deductible against rental and other income, depending on the circumstances.

- No guaranteed refund: tax outcomes depend on income, deductions, records and personal circumstances.

- Records matter: you need income and expense records that support the rental loss you report.

- General information only: this guide is not tax, legal or financial advice.

Part of the rental property tax guide hub

Use the Rental Property Tax Guide to read this with the income, deductions, depreciation and tax return checklist guides.

Negative gearing is a tax result, not a promise of profit. In plain English, a rental property is negatively geared when the deductible costs of the rental property are more than the rental income it produces.

The ATO’s Other tax considerations section explains that negative gearing occurs when you buy a rental property with borrowed funds and the rental income is less than the deductible expenses, including interest on the borrowings.

This guide explains the concept for Australian landlords. It is general information only and is not tax advice.

What negative gearing means

The simplest way to understand negative gearing is:

rental income - deductible rental expenses = net rental income or loss

If income is more than deductible expenses, there is net rental income. If deductible expenses are more than income, there is a net rental loss.

The ATO says the tax result of negatively gearing a property is that a net rental loss arises. In that case, you may be able to claim a deduction for the full amount of rental expenses against your rental and other income, such as salary, wages or business income, when completing the relevant tax return. If other income is not sufficient to absorb the loss, the ATO says it can be carried forward to the next income year.

The words “may be able to” matter. The final result depends on the deductions being allowable, correctly apportioned and supported by records.

The 2026-27 Federal Budget announced negative gearing changes from 1 July 2027. The Budget material says existing arrangements remain unchanged for properties held before 7:30 pm AEST on 12 May 2026, and investors in new builds will still be able to deduct losses from other income. For established residential properties bought after Budget night, losses are expected to be limited to residential property income, with unused losses carried forward. Because commencement, legislation and personal circumstances matter, check current ATO or Budget guidance or speak with a registered tax agent before relying on any negative gearing outcome.

Negative gearing vs cash flow

Negative gearing is a tax concept based on rental income and deductible expenses. Cash flow is a budgeting view of money coming in and going out.

Those views can differ. For example, some tax deductions relate to decline in value or capital works over time rather than a fresh cash payment in the current week. On the other hand, some cash outflows may not be deductible rental expenses.

Use the rental property cash flow calculator to understand your money-in, money-out position. Use the negative gearing calculator as a planning tool to estimate a tax-position view. Then check current ATO guidance or speak with a registered tax agent before relying on the result.

What goes into a negative gearing calculation

Start with the ATO’s rental property worksheet logic: rent and other rental-related income, less rental property expenses, produces net rental income or loss.

Common expense categories in the ATO material include:

- advertising for tenants

- body corporate fees and charges

- council rates and water charges

- insurance

- interest on loans

- land tax

- legal expenses

- pest control

- property agent fees and commission

- repairs and maintenance

- deductions for decline in value

- capital works deductions.

Some expenses may be immediate deductions. Some may be claimed over several years. Some may not be claimable. For the broader deduction overview, read Rental Property Tax Deductions Australia.

Why interest and borrowing records matter

The ATO’s negative gearing explanation specifically refers to borrowed funds and interest on borrowings. The ATO rental expenses guidance also notes that some borrowing expenses are claimed over several years.

That makes loan records important. Keep loan documents, interest statements and evidence that separates rental-property borrowing from any private use of funds. If a loan account is used for both rental property and private purposes, the ATO material says interest must be apportioned into deductible and non-deductible parts according to the amounts borrowed for each purpose.

Co-owners need to use the right share

The ATO says rental income and expenses are generally reported according to legal ownership. For example, if you own 50% of a property, you must declare 50% of the rental income.

The ATO Rental Properties Guide also gives examples showing that co-owners who are not carrying on a business of letting rental properties divide income and expenses in line with their legal interest. A private agreement to shift more of the rental loss to the higher-income owner does not change that income tax treatment in the ATO example.

This is an area to confirm with a registered tax agent if ownership, trusts, companies, partnerships or business activity are involved.

Use a negative gearing calculator carefully

A negative gearing calculator can help you model a rental property, but it is only as good as the inputs.

Before using one, gather:

- rent and other rental-related income

- interest on loans

- council rates, water charges, insurance and land tax

- property agent fees or self-management costs

- repairs and maintenance

- depreciation and capital works estimates

- ownership percentage

- any periods of private use, below-market rent or vacancy issues that affect deductibility.

Try the Landlord Wise negative gearing calculator to model a scenario. It is a planning tool, not tax advice and not a tax return.

PAYG withholding and timing

The ATO also notes that if you believe your circumstances warrant a reduction to your rate or amount of withholding, you can apply to the ATO for a PAYG withholding variation. That is separate from deciding whether a rental expense is deductible. Treat it as an ATO/tax-agent conversation, not a calculator output.

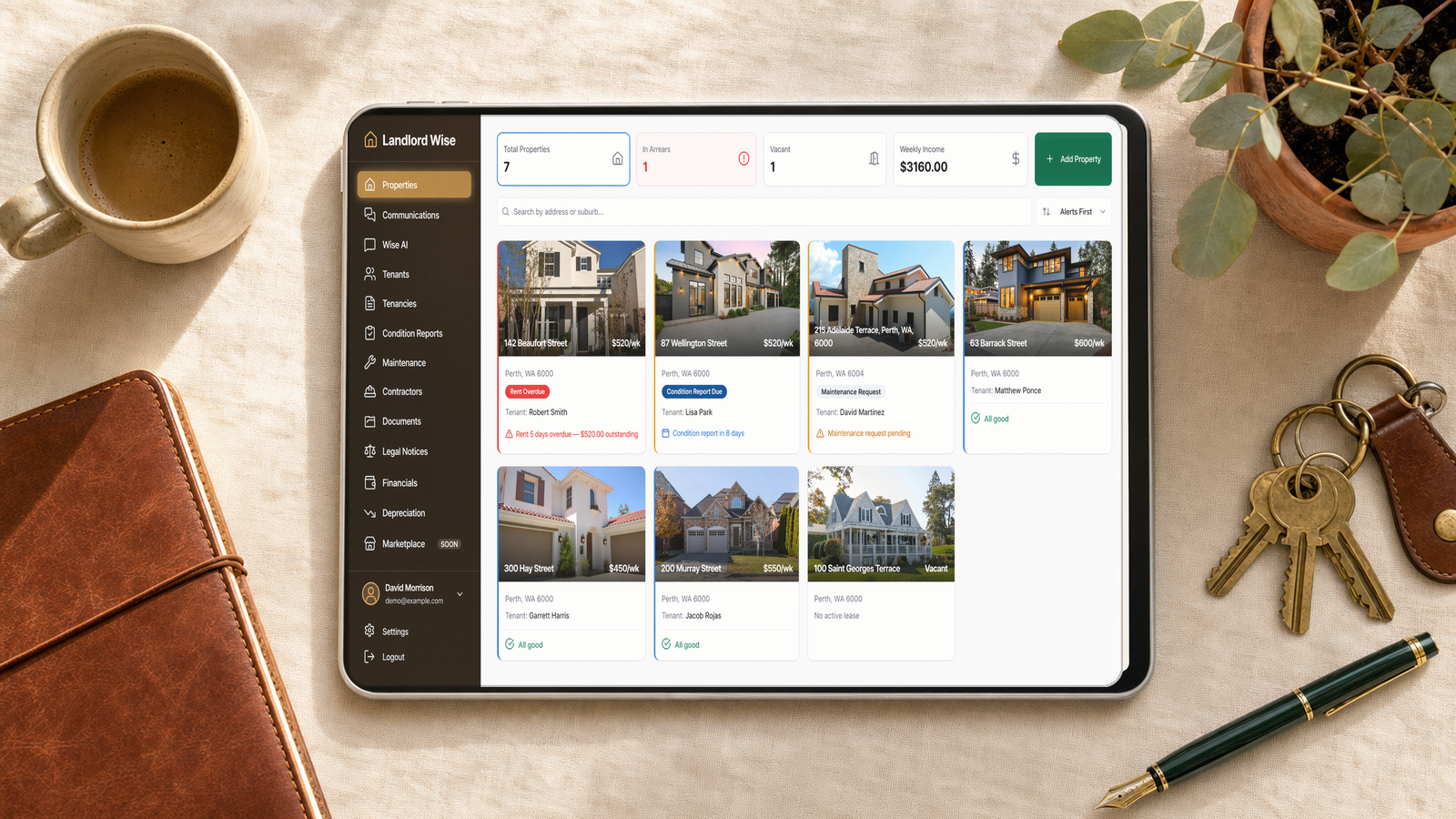

How Landlord Wise helps landlords prepare

Landlord Wise helps self-managing landlords keep the records that make tax time easier:

- rent tracking by property and tenancy

- expense records and receipt storage

- document storage for leases, invoices and statements

- tools for depreciation, negative gearing, cash flow and yield

- tenancy workflows, condition reports and maintenance records in the same platform.

The goal is organisation. Landlord Wise does not guarantee deductions, calculate your final taxable income, lodge your tax return or replace a tax agent.

Frequently Asked Questions

What is negative gearing in Australia?

The ATO explains that negative gearing occurs when you buy a rental property with borrowed funds and the rental income is less than the deductible expenses, including interest on borrowings.

Does negative gearing guarantee a tax refund?

No. The ATO says a net rental loss may arise and may be deducted against rental and other income, but the actual tax result depends on the taxpayer’s circumstances. Do not treat a calculator estimate as a guaranteed refund.

Can a rental loss be carried forward?

The ATO says that where other income is not sufficient to absorb the rental loss, it can be carried forward to the next income year.

Is negative gearing the same as negative cash flow?

No. Negative gearing is a tax-position concept based on rental income and deductible expenses. Cash flow is a budgeting view of actual money coming in and out.

What records do I need for negative gearing?

You need rent and rent-related income records, expense records, loan documents, receipts, bank statements and records that support ownership shares and any apportionment.

Related guides and tools

- Negative gearing calculator

- Rental Property Tax Deductions Australia

- Rental Property Depreciation Australia

- Rental Income Tax Australia

- Rental Property Tax Return Checklist

- Rental property cash flow calculator

- Rental yield calculator

Disclaimer

This guide is general information for Australian residential landlords. It is not tax, legal or financial advice. Negative gearing outcomes depend on your circumstances and the deductions you can substantiate. Check current ATO guidance and speak with a registered tax agent before making tax decisions. Landlord Wise helps organise records and model scenarios, but it does not give tax advice or lodge tax returns.

Related Guides

Most useful next-step guides for landlords.

Rental Property Tax Deductions Australia: Guide for Landlords

Plain-English guide to rental property tax deductions in Australia, including income, common expenses, depreciation, capital works and record keeping.

Rental Property Depreciation Australia: How to Calculate It

Learn the ATO-backed basics of rental property depreciation in Australia, including depreciating assets, capital works, second-hand asset limits and records.

Rental Income Tax Australia: What Landlords Need to Declare

Guide for Australian landlords on rental income tax, what the ATO says to declare, common rental income types and record keeping.

Rental Property Tax Return Checklist for Australian Landlords

EOFY rental property tax return checklist for Australian landlords, covering income records, expenses, repairs, depreciation, ownership and ATO record keeping.

How to Self-Manage a Rental Property in Australia (2026 Guide)

Learn how to self-manage a rental property in Australia, including tenant screening, leases, bonds, condition reports, rent records, maintenance and state rules.

Keep rental income, expenses, receipts and EOFY records together

Landlord Wise is free during early access. Use it to organise rent income, expenses, receipts, documents and property records before tax time.