Free early access

Keep rental income, expenses, receipts and EOFY records together

Landlord Wise is free during early access. Use it to organise rent income, expenses, receipts, documents and property records before tax time.

At a glance

- Depreciating assets: the ATO describes these as plant items that do not form part of the building structure.

- Capital works: the ATO treats building construction, structural improvements, alterations and extensions separately.

- Methods: the ATO explains diminishing value and prime cost methods for decline in value.

- Second-hand limits: in most cases, the ATO says you cannot claim a deduction for second-hand depreciating assets after 1 July 2017.

- General information only: confirm depreciation treatment with current ATO guidance or a registered tax agent.

Part of the rental property tax guide hub

Use the Rental Property Tax Guide to read depreciation alongside income, deductions, negative gearing and tax return records.

Rental property depreciation is the process of claiming the decline in value of eligible rental property assets over time. For landlords, it is one of the more technical parts of a rental property tax return because the ATO treats assets, capital works, repairs and improvements differently.

This guide is grounded in the ATO source pack, especially the ATO pages on depreciating assets in rental properties and capital expenses. It is general information only and not tax advice.

Depreciating assets in rental properties

The ATO says depreciating assets are items that can be described as plant and do not form part of the rental property’s premises. Premises means the actual structure of the rental property’s building.

The ATO says depreciating assets are usually:

- separately identifiable

- unlikely to be permanent

- replaced within a relatively short period

- not part of the structure of the building.

Examples in the ATO source material include floating timber flooring, carpets, curtains, appliances such as a washing machine or fridge, and furniture.

For depreciating assets used for income-producing purposes, you may be able to claim a deduction for decline in value. The ATO says you can use either the Commissioner’s effective life or your own reasonable estimate of the effective life, and that you must keep records showing how you work out the decline in value.

Capital works are different

Capital works are not the same as depreciating assets. The ATO says capital works include expenses for building the property and structural improvements, alterations and extensions.

Examples of capital works expenses in the ATO material include:

- building and construction costs

- alterations to a building

- major renovations to a room

- substantial renovations to a property

- adding a fence

- building extensions such as garages and patios

- adding structural improvements such as a driveway or retaining wall.

The ATO says the capital works deduction rate is generally 2.5% or 4% per year, spread over 40 or 25 years respectively, and that capital works deductions cannot exceed construction expenses.

How decline in value is calculated

The ATO explains two methods for calculating deductions for decline in value:

- the diminishing value method, where the decline in value each year is a constant portion of the remaining value, producing higher deductions in the early years of the asset’s effective life

- the prime cost method, where the decline in value each year is a uniform amount of the original value over the asset’s effective life.

The ATO source material gives formulas for both methods:

| Method | ATO formula | What the percentage means |

|---|---|---|

| Diminishing value | Base value x (days held / 365) x (200% / asset’s effective life) | 200% means 2.0 divided by the asset’s effective life. A 10-year asset has a 20% diminishing value rate for a full year. |

| Prime cost | Asset’s cost x (days held / 365) x (100% / asset’s effective life) | 100% means 1.0 divided by the asset’s effective life. A 10-year asset has a 10% prime cost rate for a full year. |

The 100% and 200% figures are just the rate numerator in the ATO formula. They do not mean you claim 100% or 200% of the asset’s cost in one year. You divide that percentage by the asset’s effective life first, then apply the days-held part of the formula.

For the diminishing value method, the ATO explains that base value is the asset’s cost in the income year the asset is first used or installed ready for use. For later income years, base value generally uses the asset’s opening adjustable value plus any second element of cost for that year. The ATO source material also notes that depreciating assets held before 10 May 2006 use 150% rather than 200% in the diminishing value formula.

These formulas are a technical starting point, not a substitute for working through your asset, date, taxable-use percentage, second-hand asset limits and records with current ATO guidance or a registered tax agent.

Use the Landlord Wise depreciation calculator to model a rental property asset. Treat the result as an estimate for planning and record organisation, then check the ATO guidance or a registered tax agent before claiming.

Assets costing $300 or less

The ATO says certain non-business depreciating assets costing $300 or less may be immediately deductible in the income year you use the asset to produce assessable income, if the ATO tests are met.

Those tests include that the asset cost $300 or less, was used mainly to produce assessable income that was not income from carrying on a business, was not part of a set of assets costing more than $300 that you started to hold in the income year, and was not one of a number of identical or substantially identical assets that together cost more than $300.

Because this rule is specific, keep purchase invoices and details of whether the item was part of a set, part of a group of identical or substantially identical assets, or a separate asset.

Low-value pools

The ATO source material says depreciating assets valued at less than $1,000 can be grouped in a low-value asset pool and depreciated together. The ATO Rental Properties Guide explains that low-value pooling has its own rules, including taxable-use percentages and special treatment for assets affected by the second-hand depreciating asset limits.

Do not assume pooling applies just because an asset is under $1,000. Keep the asset records and check the ATO’s depreciating asset guidance or your registered tax agent.

New vs second-hand depreciating assets

The ATO says you can claim the decline in value of new depreciating assets.

For second-hand assets, the source pack is more restrictive. The ATO says that in most cases you cannot claim a deduction for second-hand depreciating assets after 1 July 2017. The ATO Rental Properties Guide also refers to certain assets acquired after 7:30 pm on 9 May 2017 when explaining the detailed limit on deductions for decline in value of second-hand depreciating assets in residential rental properties.

That means landlords should be careful with established properties. A carpet, appliance or air conditioner that came with a property may not be treated the same as a brand-new asset you bought and installed for the rental property.

Quantity surveyors and depreciation schedules

The ATO says a quantity surveyor can prepare a report at the time a rental property is purchased. The ATO also recommends keeping a spreadsheet as a minimum for depreciating assets as part of your record keeping.

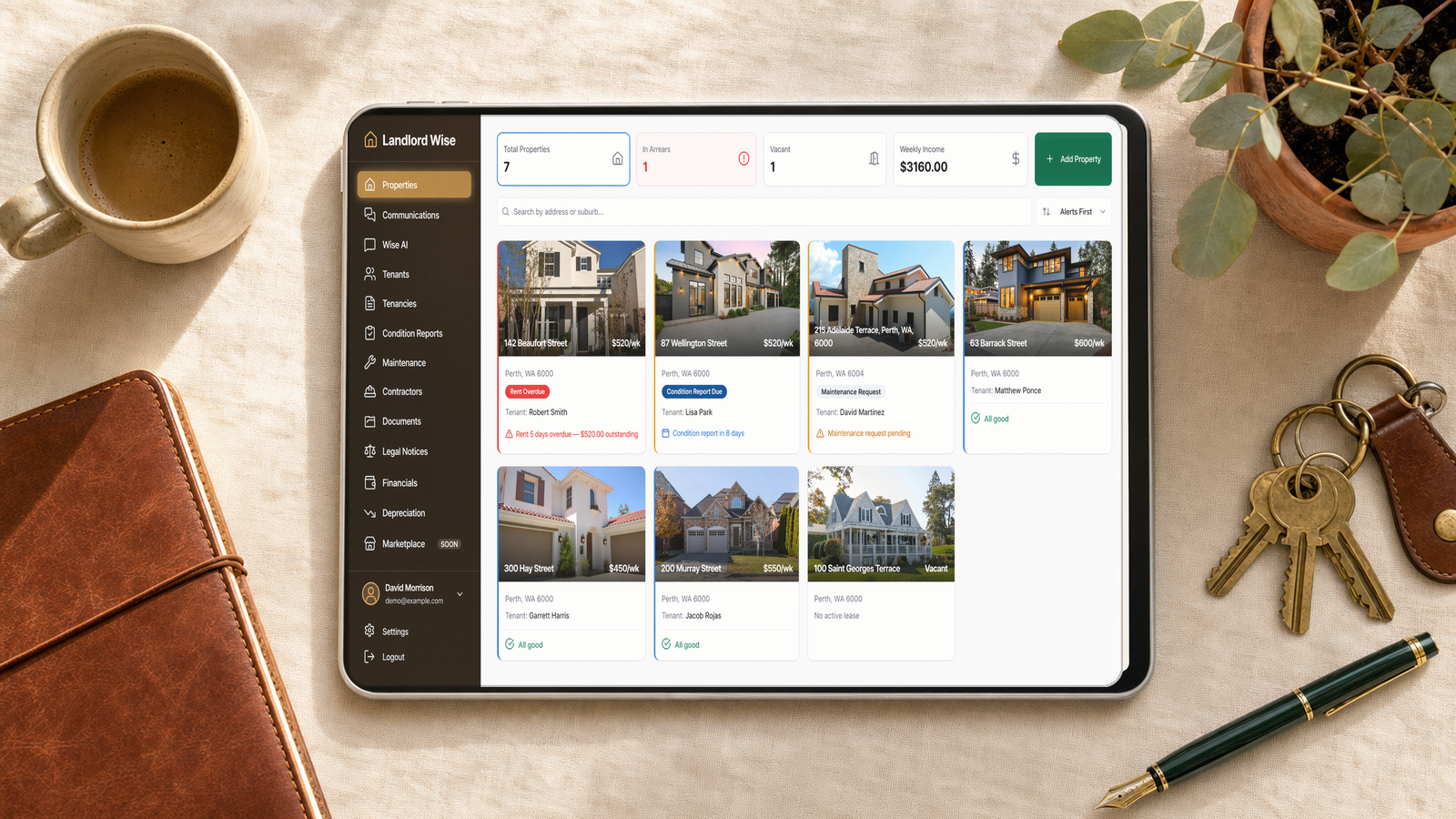

Landlord Wise can help organise asset records, purchase dates, documents and rental property expenses. It does not replace a quantity surveyor, registered tax agent or ATO depreciation tool.

Depreciation and negative gearing

Depreciation can affect your net rental income or loss because it is part of the rental expense picture. The ATO’s rental property worksheet includes deductions for decline in value and capital works deductions as expense lines when working out net rental income or loss.

If you are modelling the broader tax position, use the negative gearing calculator and read Negative Gearing Explained for Australian Landlords. Do not assume that a depreciation estimate means a deduction is available in your personal circumstances.

Frequently Asked Questions

What is rental property depreciation?

Rental property depreciation generally refers to claiming decline in value for eligible depreciating assets, and separately claiming eligible capital works over time.

What is the difference between depreciating assets and capital works?

The ATO describes depreciating assets as plant items that do not form part of the building structure. Capital works include building construction and structural improvements, alterations and extensions.

Can I claim second-hand assets in a rental property?

The ATO says that in most cases you cannot claim a deduction for second-hand depreciating assets after 1 July 2017. The detailed rule also refers to certain assets acquired after 7:30 pm on 9 May 2017. Check the current ATO guidance and your circumstances before claiming.

Do I need a depreciation schedule?

The ATO source pack says a quantity surveyor can prepare a report at the time a rental property is purchased and recommends keeping a spreadsheet as a minimum for depreciating assets. Whether you need a formal schedule depends on your property and circumstances.

Does Landlord Wise calculate my final depreciation claim?

No. Landlord Wise provides tools and record organisation. It does not give tax advice, prepare quantity surveyor reports or lodge tax returns.

Related guides and tools

- Depreciation calculator

- Rental Property Tax Deductions Australia

- Negative Gearing Explained

- Rental Property Tax Return Checklist

- Rental property cash flow calculator

- All Landlord Wise calculators

Disclaimer

This guide is general information for Australian residential landlords. It is not tax, legal or financial advice. Depreciation and capital works claims depend on the asset, property, dates, ownership, use and records. Check current ATO guidance and speak with a registered tax agent or qualified depreciation professional before deciding what to claim. Landlord Wise helps organise records and provide planning tools, but it does not replace professional tax advice.

Related Guides

Most useful next-step guides for landlords.

Rental Property Tax Deductions Australia: Guide for Landlords

Plain-English guide to rental property tax deductions in Australia, including income, common expenses, depreciation, capital works and record keeping.

Negative Gearing Explained for Australian Landlords

Plain-English guide to negative gearing in Australia, how net rental losses work, what records landlords need and how to use a negative gearing calculator carefully.

Rental Property Tax Return Checklist for Australian Landlords

EOFY rental property tax return checklist for Australian landlords, covering income records, expenses, repairs, depreciation, ownership and ATO record keeping.

Rental Income Tax Australia: What Landlords Need to Declare

Guide for Australian landlords on rental income tax, what the ATO says to declare, common rental income types and record keeping.

How to Self-Manage a Rental Property in Australia (2026 Guide)

Learn how to self-manage a rental property in Australia, including tenant screening, leases, bonds, condition reports, rent records, maintenance and state rules.

Keep rental income, expenses, receipts and EOFY records together

Landlord Wise is free during early access. Use it to organise rent income, expenses, receipts, documents and property records before tax time.