Free early access

Keep rental income, expenses, receipts and EOFY records together

Landlord Wise is free during early access. Use it to organise rent income, expenses, receipts, documents and property records before tax time.

At a glance

- Start with income: the ATO says landlords must declare rental income and related payments.

- Then categorise expenses: some rental expenses may be claimed in the year incurred, while others are claimed over several years.

- Watch the limits: private use, vacant land, below-market rent, capital expenses and second-hand depreciating assets can change what you can claim.

- Keep records: the ATO expects income and expense records that can support your tax return.

- General information only: use this guide to organise questions for the ATO or a registered tax agent.

Part of the rental property tax guide hub

Use the Rental Property Tax Guide to browse income, deductions, depreciation, negative gearing and tax-time checklist articles together.

Rental property tax deductions in Australia are not a single blanket claim. The practical workflow is to declare your rental income, separate expenses by type, keep evidence, and check whether each cost is claimable now, claimable over time, or not claimable.

The ATO’s Rental properties guide 2025 is the main source for this guide. This article is general information only. It is not tax advice and Landlord Wise does not lodge tax returns or decide what you should claim.

Rental income comes first

Before deductions, the ATO explains that you must declare income you receive from renting, leasing or licensing your rental property. That can include ordinary rent, short-term rental income, renting part or all of your home, and some arrangements involving family or friends.

The ATO also says rental income can include payments in cash or in the form of goods and services, bond money retained in place of rent or because of damage, letting or booking fees, insurance payouts for damage or loss of rent, payments from tenants for deductible expenses, government rebates for depreciating assets, and lump sum rental income.

For more detail, see the ATO page on rental income you must declare and our companion guide, Rental Income Tax Australia.

Immediate deductions vs deductions over time

The ATO separates rental property expenses into broad groups:

- expenses you may be able to claim in the income year you incur them

- expenses you may need to claim over several years

- expenses you cannot claim as a deduction.

The ATO gives examples of expenses that may be claimable in the year incurred, including interest on loans, council rates, repairs and maintenance, and depreciating assets costing $300 or less.

The ATO also gives examples of expenses that are claimed over several years, including capital works, borrowing expenses, and the decline in value of depreciating assets costing more than $300.

Some costs may not be claimable as rental deductions. The ATO examples include personal expenses, expenses from personal use of the property, some capital expenses, and certain second-hand depreciating assets. The ATO source material refers to restrictions applying from 1 July 2017 and to certain assets acquired after 7:30 pm on 9 May 2017, so check the detailed ATO rule before claiming.

That is why a clean category system matters. “Property expense” is too broad for tax time. You need enough detail to separate repairs from improvements, interest from principal, capital works from ordinary running costs, and private use from income-producing use.

What landlords generally cannot claim

The ATO also names limits that landlords should not miss:

- travel expenses that relate to a residential rental property are not deductible unless an exception applies

- holding costs for vacant land are generally not deductible before the property can be occupied and is available for rent, unless an exception applies

- decline in value deductions for certain second-hand depreciating assets in residential rental properties are limited, unless an exception applies.

These limits are not minor details. They can change the treatment of costs that look like ordinary property expenses, so keep the source records and check the ATO rule before lodging.

Common rental property expenses

The ATO’s common property expenses page lists examples of rental expenses that may be immediately deductible where the property is held to produce assessable income on commercial terms.

Examples include:

- advertising for tenants

- body corporate administrative fund fees and charges

- council rates, water charges and land tax

- cleaning, gardening and lawn mowing

- pest control

- insurance, including building, contents, public liability and loss of rent

- interest expenses

- property agent fees and commission

- repairs and maintenance

- some legal expenses.

These are categories, not automatic approvals. The ATO says you must actually incur the cost and keep adequate records to prove deductions if asked.

Repairs, maintenance and capital work

Repairs and maintenance are one of the areas where landlords can easily misclassify expenses.

The ATO says repair and maintenance expenses are costs you incur to keep the property in a tenantable condition, or to fix wear and tear or damage that occurs while renting out the property.

But some repair-like work is capital in nature and must be treated differently. The ATO identifies initial repairs for defects that existed when you acquired the property, improvements, and replacement of entire units of property as examples that may need capital treatment rather than immediate deduction treatment.

For the detail, compare the ATO pages on repair and maintenance expenses and capital expenses.

Depreciating assets and capital works

The ATO treats depreciating assets and capital works as separate concepts.

Depreciating assets are items that can be described as plant and do not form part of the rental property’s building structure. The ATO examples include items such as carpets, curtains, appliances, furniture and floating timber flooring.

Capital works include building construction costs, structural improvements, alterations and extensions. The ATO says capital works deductions are generally spread over time and cannot exceed construction expenses.

If you are working through this area, start with our rental property depreciation guide and the depreciation calculator. Use those as organising tools, then check the ATO guidance or a registered tax agent before deciding what to claim.

Apportionment and private use

The ATO says expenses may need to be apportioned if:

- the property is only held to produce assessable rental income for part of the year

- the property is vacant land for part of the year

- the property is used privately or personally for part of the year

- only part of the property is rented

- rent is charged below market rates

- an investment loan is also used for private purposes.

For a normal long-term rental property used only to earn rent, apportionment may be less complicated. For short-term rentals, shared homes, family arrangements, holiday homes or mixed-use loans, it can become much more important.

How Landlord Wise helps at tax time

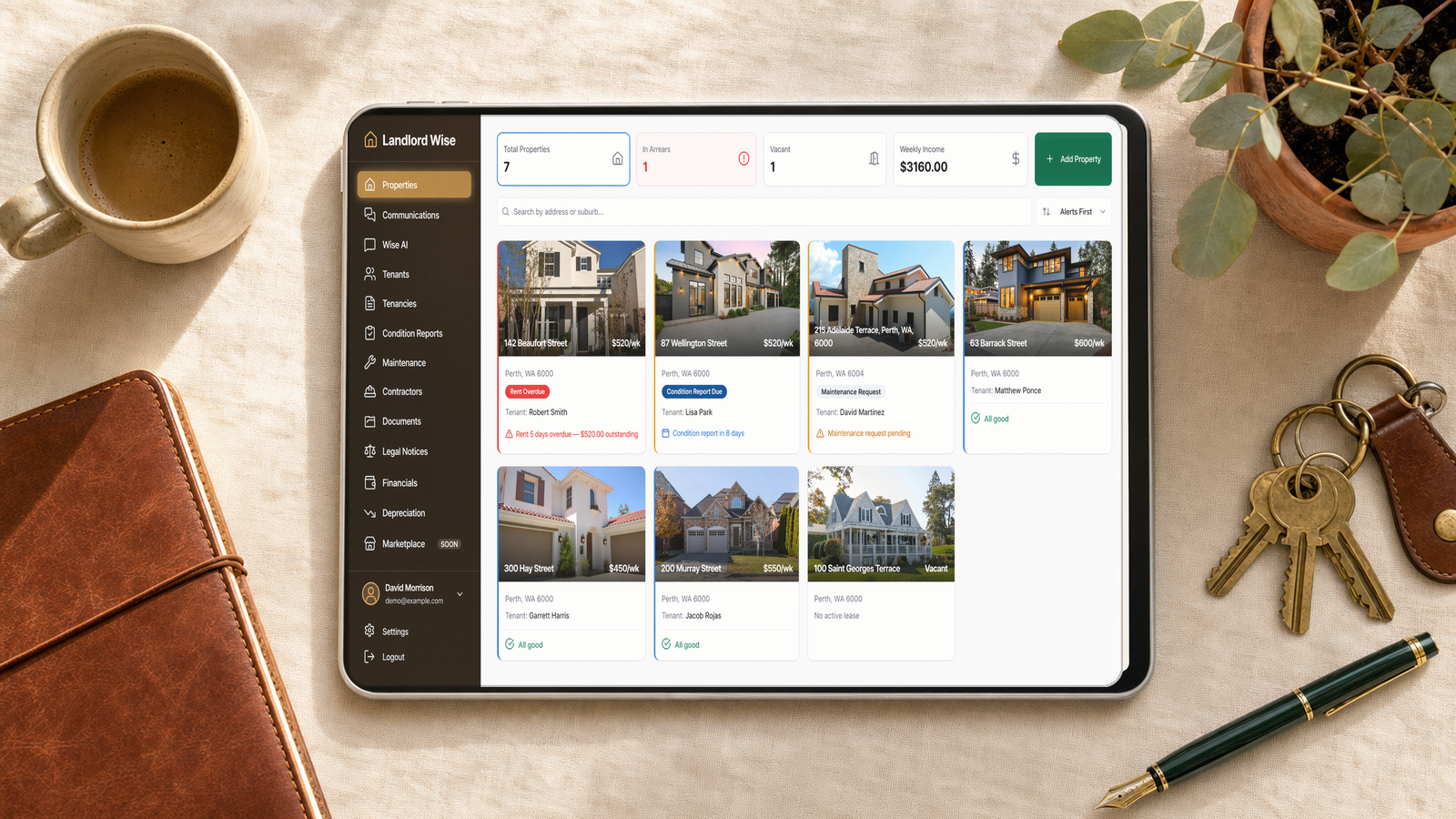

Landlord Wise helps landlords keep the practical records behind these tax categories. You can track rent income, record expenses, store receipts and documents, organise property records, and keep tenancy workflows in the same place.

The public tools can also help you prepare questions for your accountant:

- Negative gearing calculator

- Depreciation calculator

- Rental property cash flow calculator

- Rental yield calculator

- Land tax calculator

These tools are for planning and organisation. They do not replace ATO guidance, a tax return, or advice from a registered tax agent.

Frequently Asked Questions

What rental property expenses can landlords claim in Australia?

The ATO lists examples such as advertising for tenants, council rates, water charges, land tax, insurance, interest expenses, property agent fees, repairs and maintenance, and some legal expenses. Whether you can claim a specific cost depends on the facts, records and tax treatment.

Are all rental property expenses deductible straight away?

No. The ATO separates expenses into those that may be claimed in the income year incurred, those claimed over several years, and those that cannot be claimed as deductions.

Can I claim renovations as a rental property deduction?

The ATO treats improvements and substantial renovations as capital expenses, not ordinary repairs. They may be claimed over time as capital works or, for some replaced items, as depreciating assets.

Do I need receipts for rental property deductions?

The ATO says you must keep adequate records to prove your deductions if asked. Expense records should include supplier, amount, nature of goods or services, date incurred and date of the document.

Can Landlord Wise tell me what deductions to claim?

No. Landlord Wise helps organise rent, expenses, documents and tax-time information. It does not provide tax advice or decide what you should claim.

Related guides and tools

- Rental Income Tax Australia

- Rental Property Tax Return Checklist

- Negative Gearing Explained

- Rental Property Depreciation Australia

- Depreciation calculator

- Negative gearing calculator

- All Landlord Wise calculators

Disclaimer

This guide is general information for Australian residential landlords. It is not tax, legal or financial advice. Tax rules depend on your circumstances and can change over time. Check current ATO guidance and speak with a registered tax agent before deciding what to claim. Landlord Wise helps organise rental property records and tax-time information, but it does not lodge tax returns or replace professional tax advice.

Related Guides

Most useful next-step guides for landlords.

Rental Income Tax Australia: What Landlords Need to Declare

Guide for Australian landlords on rental income tax, what the ATO says to declare, common rental income types and record keeping.

Rental Property Tax Return Checklist for Australian Landlords

EOFY rental property tax return checklist for Australian landlords, covering income records, expenses, repairs, depreciation, ownership and ATO record keeping.

Negative Gearing Explained for Australian Landlords

Plain-English guide to negative gearing in Australia, how net rental losses work, what records landlords need and how to use a negative gearing calculator carefully.

Rental Property Depreciation Australia: How to Calculate It

Learn the ATO-backed basics of rental property depreciation in Australia, including depreciating assets, capital works, second-hand asset limits and records.

How to Self-Manage a Rental Property in Australia (2026 Guide)

Learn how to self-manage a rental property in Australia, including tenant screening, leases, bonds, condition reports, rent records, maintenance and state rules.

Keep rental income, expenses, receipts and EOFY records together

Landlord Wise is free during early access. Use it to organise rent income, expenses, receipts, documents and property records before tax time.